{kind=link}

Simply sign up to the German economy myFT Digest — delivered directly to your inbox.

“Germany is struggling. It was the only G7 economy to shrink last year and is set to be the group’s slowest-growing economy again this year.” These are the opening words of a blog by members of the IMF’s European Department published on March 27. According to the IMF, its GDP per head shrank 1 per cent between 2019 and 2023. This was the 34th-worst outcome out of 41 high-income economies. Of G7 economies, only Canada did worse. Even the UK, with a decline of 0.2 per cent, and France, with a small rise of 0.4 per cent, did better. The US rise of 6 per cent was in another league.

If Germany has recently been a sick man, is this a temporary or a chronic condition? There are good reasons for arguing it is mainly the former. As the blog notes, Germany’s terms of trade deteriorated hugely after Russia’s invasion of Ukraine, as the price of natural gas soared. But the terms of trade have returned to 2018 levels as the price of natural gas fell once again. The concomitant spike in inflation has reversed and ECB monetary policy has started to ease. Finally, the post-pandemic rebalancing of global demand from manufactured goods towards services was also unfavourable for Germany’s economy. But this, too, is set to reverse.

The IMF adds that concerns for the longer-term future of German industry are exaggerated. Yes, energy-intensive industries have contracted, but they only account for 4 per cent of the economy. Automobile production, by contrast, rose 11 per cent in 2023, while electric vehicle exports rose 60 per cent. Moreover, it adds, “manufacturing value-added has remained steady even as industrial production has fallen”.

According to the July Consensus Forecasts, German growth is expected to be a mere 0.2 per cent in 2024. But it is forecast to reach 1.1 per cent next year. Yet if that is to be the new normal, it is rather a poor one. It is these long-run trends rather than recent shocks that are the big issue. The German economy suffers from five adverse trends.

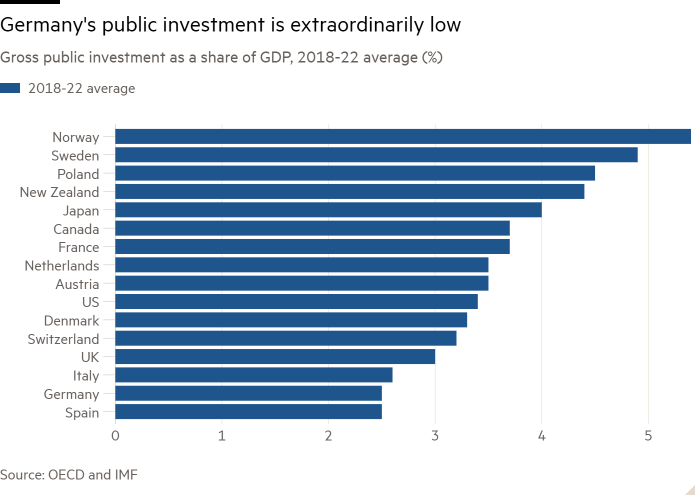

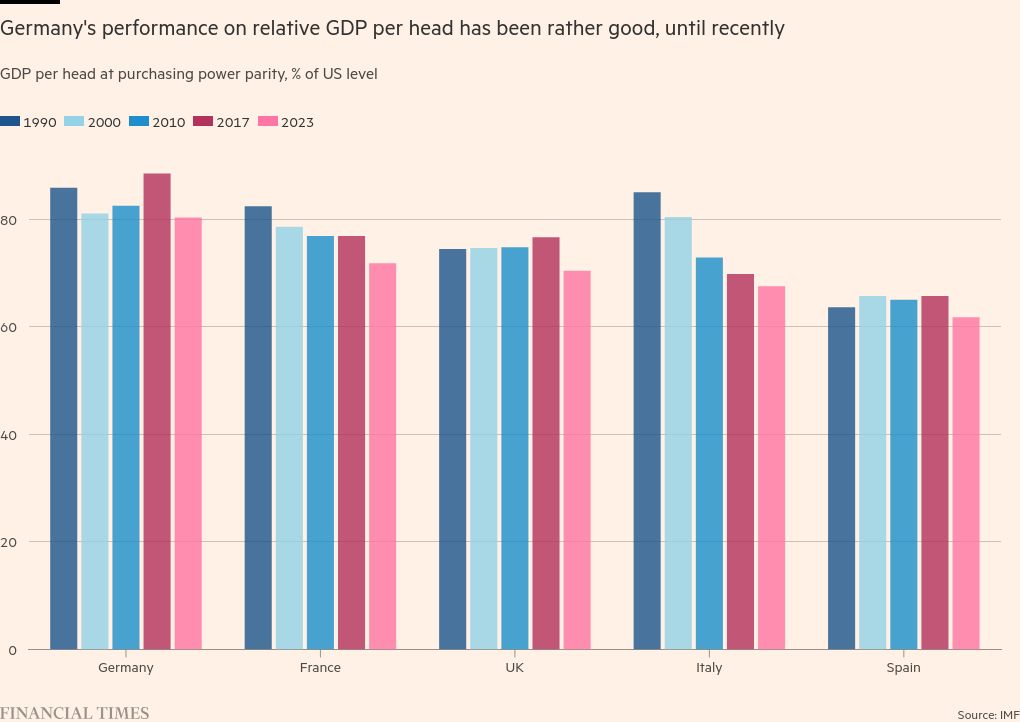

First, the growth of Germany’s labour force (people aged 15-64) is forecast to fall by 0.66 percentage points between 2025 and 2029, relative to growth between 2019 and 2023. This is the biggest such fall in the G7. Second, the share of gross public investment in GDP, which was 2.5 per cent from 2018 to 2022, was the lowest among significant high-income countries, apart from Spain. It was even below the UK’s rather poor 3 per cent. Third, Germany’s GDP per head (at purchasing power parity) declined from 89 per cent of US levels in 2017 to 80 per cent in 2023. This was the largest relative decline of any G7 member over that period. Fourth, Germany continues to play an insignificant role in the digital economy. Since it is Europe’s largest economy, that matters for the EU as a whole, too. Finally, the world is moving into an era of fragmentation. This will be particularly significant for Germany’s relatively trade-dependent economy.

These are significant headwinds, all of which need to be considered and addressed. But none of them will be particularly surprising. Openness to immigration, reductions in red tape and creation of a European single market, with a dynamic and integrated capital market union, are all parts of the answer.

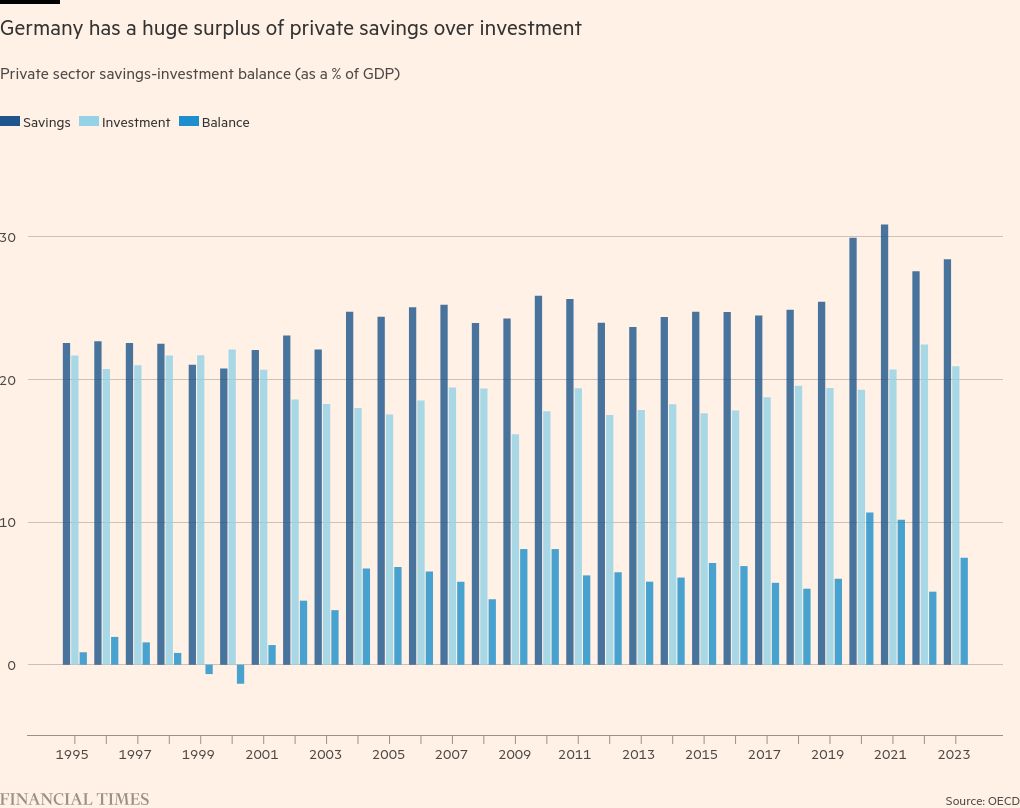

Yet there is another feature that is almost never viewed as a problem in “respectable circles” in Germany, or elsewhere: its huge structural savings surpluses, which have, of course, financed its huge current account surpluses. Many German economists view these as proof of Germany’s international competitiveness and insist that everybody else, especially in the Eurozone, should follow its example. This is nonsense.

The first reason is that everybody else cannot follow its example. Globally, savings and investment have to match. So, if one economy saves far more than it invests, others have to do the reverse. This will then be shown in its accumulation of financial claims on the deficit countries, predominantly as debt.

This German hostility to debt is folly or, worse, hypocrisy. Its surpluses must be balanced by others’ deficits and debts. Moreover, calls for Eurozone members to reduce their fiscal deficits will only work well if the current account of the euro area goes even more into surplus or private sectors in other Eurozone members (France, for example) are forced into deficit. The danger is that such adjustments will be viewed as “beggar-my-neighbour” recessions caused by Germany. That happened to the Eurozone with almost lethal ferocity in the 2010s. It must not do so again, especially given today’s febrile politics.

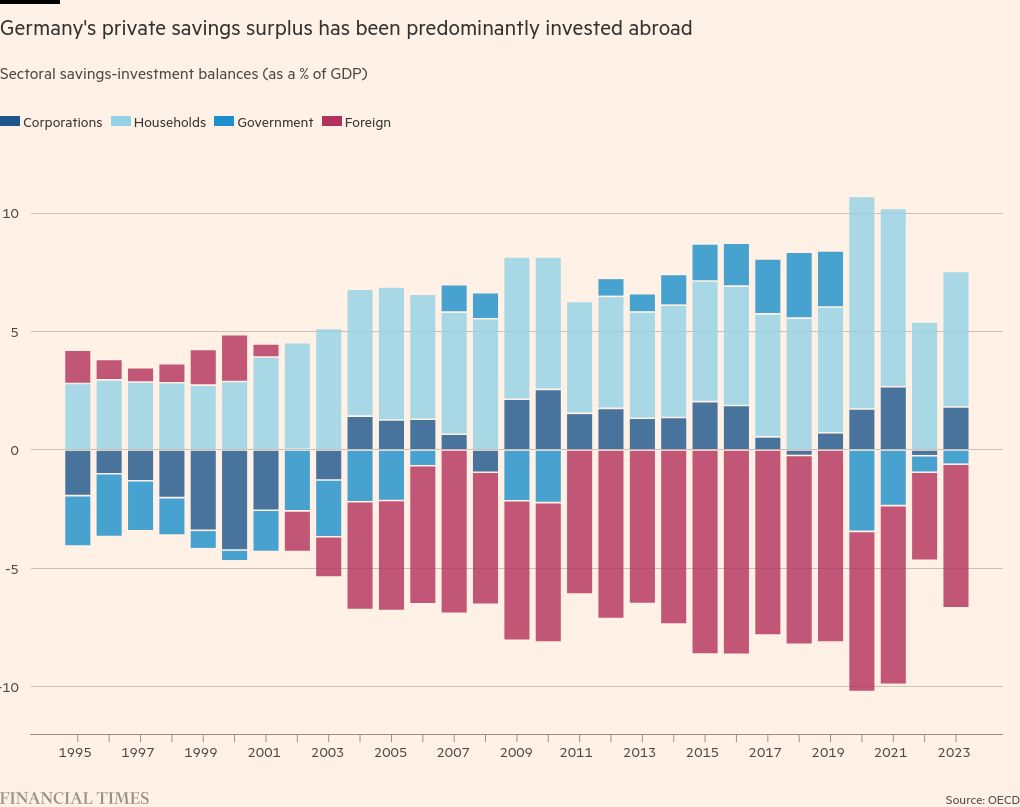

The second reason is that there is a simple domestic solution. Germany should use more of its surplus savings at home. The obvious way to do so is to raise its ultra-low level of public investment by letting the German government, one of the most creditworthy in the world, borrow from the people who trust it most, namely the German public, in order to invest more at home.

An excellent chapter on “Public Investment in Germany”, in a recent book about European public investment, notes that net public investment has been close to zero since the beginning of this century. Thus, the ratio of public capital to GDP has been consistently falling. It makes no sense for a country with such vast surplus savings in its private sector not to use them at home, thereby generating both a stronger supply side and the demand that Germany and the Eurozone will need.

Germany’s short-term problems will pass. Its longer-term ones are more challenging. But the most unnecessary one is its reluctance to fund needed public investment at home. The time to repeal the absurd “debt brake” in the constitution is now.

Follow Martin Wolf with myFT and on Twitter

Source link : https://www.ft.com/content/2135f8c7-dd60-463c-9bd5-5a907d5f8f1e

Author :

Publish date : 2024-07-16 16:24:50

Copyright for syndicated content belongs to the linked Source.