{kind=link}

Anyone looking for a parody of fiscal policy needs to look no further than France. The French government has been in breach of the EU’s fiscal rules for more than 20 years—obviously without suffering any punishment from Brussels—and the country’s political leadership takes an attitude to it that best belongs in a film by Jacques Tati.

On September 18th, France24 reported that

France was placed on a formal procedure for violating European Union budgetary rules before [Michel] Barnier was picked as head of government [earlier] this month … And the Bank of France warned this week that a projected return to EU deficit rules by 2027 was “not realistic”.

With this in mind, and with an expected deficit of 6% in the consolidated public sector next year, what does Prime Minister Barnier have to say about it? According to France 24,

I am discovering that the country’s budgetary situation is very serious … This situation requires more than just pretty statements. It requires responsible action.

It is reassuring to hear that Mr. Barnier is “discovering” a fiscal reality that has been glaringly visible in public finance statistics since at least 2002: despite some of the highest taxes in the world, the French government uses more and more borrowed money to pay its bills. Maybe if Barnier gets a few more months under his belt, he might proceed to “discovering” that his country’s fiscal recalcitrance is jeopardizing the very future of the euro zone itself.

Somewhere along the way, Barnier discovered a new finance minister, Antoine Armand. Contributing to the talk-but-no-action attitude that is endemic to French politics, on September 24th, rfi.fr reported Finance Minister Armand as promising

that he would engage with economic stakeholders, including unions and employers’ organisations in an effort to reduce government overspending. … “Apart from one or two one-off crisis years in the past 50 years, we have one of the worst deficits in our history”

According to the same article, Prime Minister Barnier made another discovery. After having categorically written off tax hikes a week earlier,

In a Sunday interview, the prime minister brought “targeted” tax rises on “wealthy people or some large companies” into play as part of a plan to improve finances.

His creative turnaround on taxes will not help instill confidence in Barnier’s government. When a relatively fresh prime minister addresses his country’s deeply pressing fiscal situation with the carefree attitude of a flip-flopper, investors have good reasons to ask if France really is a credible debtor.

As a sign that such senses are not just speculative, on September 27th France24 reported:

And just this week the yield on France’s debt—the return investors can expect for holding 10-year government bonds—outstripped the measure for Spain for the first time since 2006, pointing to falling confidence among investors.

In so many words: the financial situation for the French government is serious, but it is definitely not new or surprising in any way. As an FYI for French politicians, let me provide the salient statistical points about French public finances.

Figure 1 reports government spending (blue), taxes (red), and government debt (gray), as a share of GDP. Since spending always exceeds taxes, the consolidated French government suffers from a chronic, and most likely politically incurable budget deficit. When the deficits are large enough, the total debt grows faster than GDP, which means that the gray ‘wall’ behind the red and blue functions also grows:

Figure 1

Source of raw data: Eurostat

In a nutshell, the French people have gotten used to getting a lot of perks from the government without having to pay the full price for them. It does not matter that the gray ‘wall’ shrinks a little bit toward the end; all that means is that French GDP for a short time has outpaced government debt. This is in all likelihood not going to be the case when we get the full set of 2024 data; I fully expect the French debt-to-GDP ratio to reach 120% before 2024 is over.

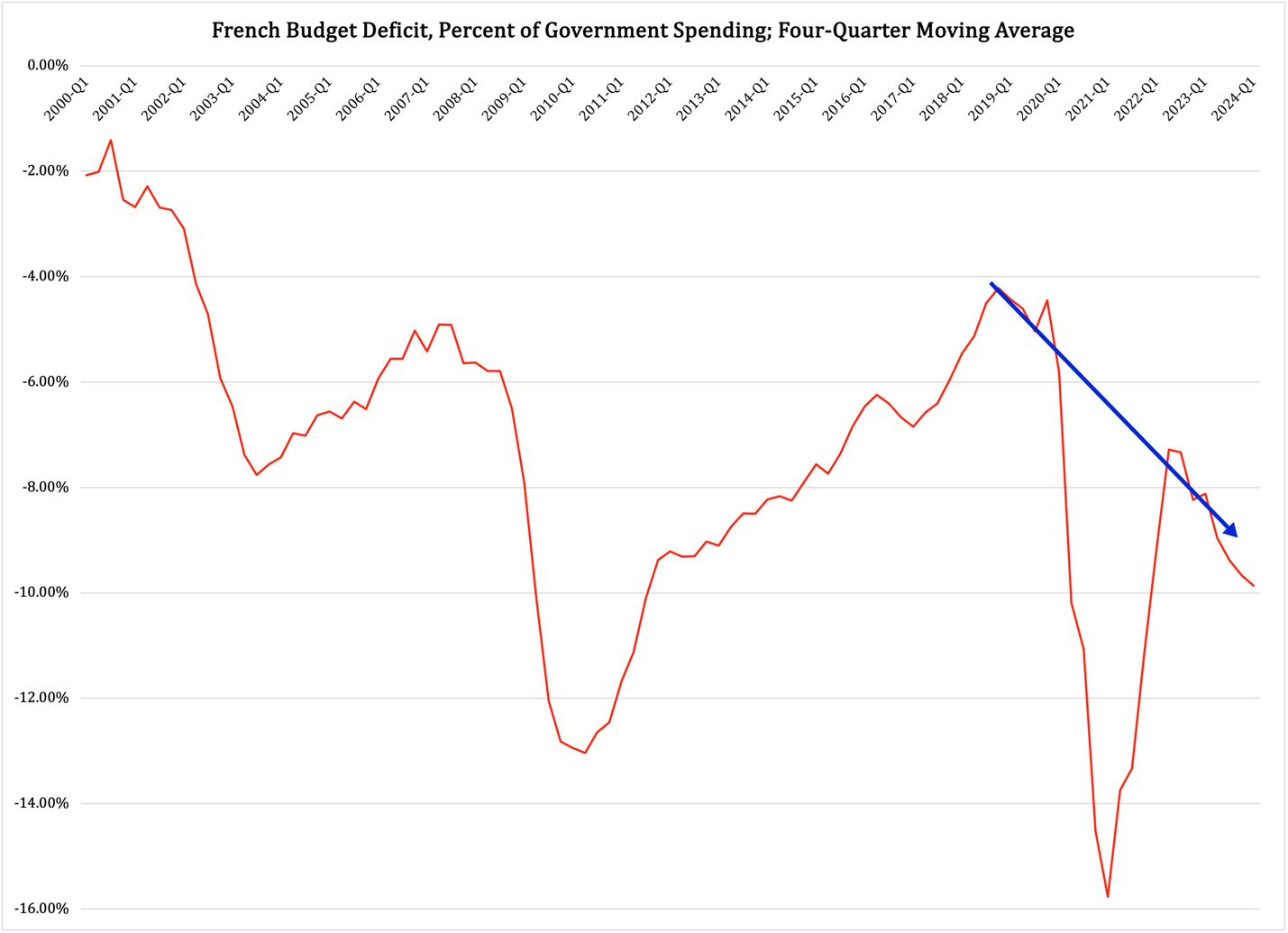

Figures 2a and 2b make two points about the budget deficit. The red function reports the deficit-to-GDP ratio, which in Figure 2a is accompanied by a short blue arrow. This arrow points to the very recent downward trend in the red function, which was concealed by the artificial circumstances around the 2020 economic shutdown. If that shutdown had not happened, the budget deficit would have been worsening pretty much along the dark blue arrow in Figure 2a:

Figure 2a

Source of raw data: Eurostat

Source of raw data: Eurostat

This trend is essential. It shows that the French government is unable to control its finances, a fact that ultimately has political roots. It is possible to reform a welfare state to such an extent that this chronic budget deficit goes away, but the politicians in charge are not willing to make the decisions necessary to break this trend.

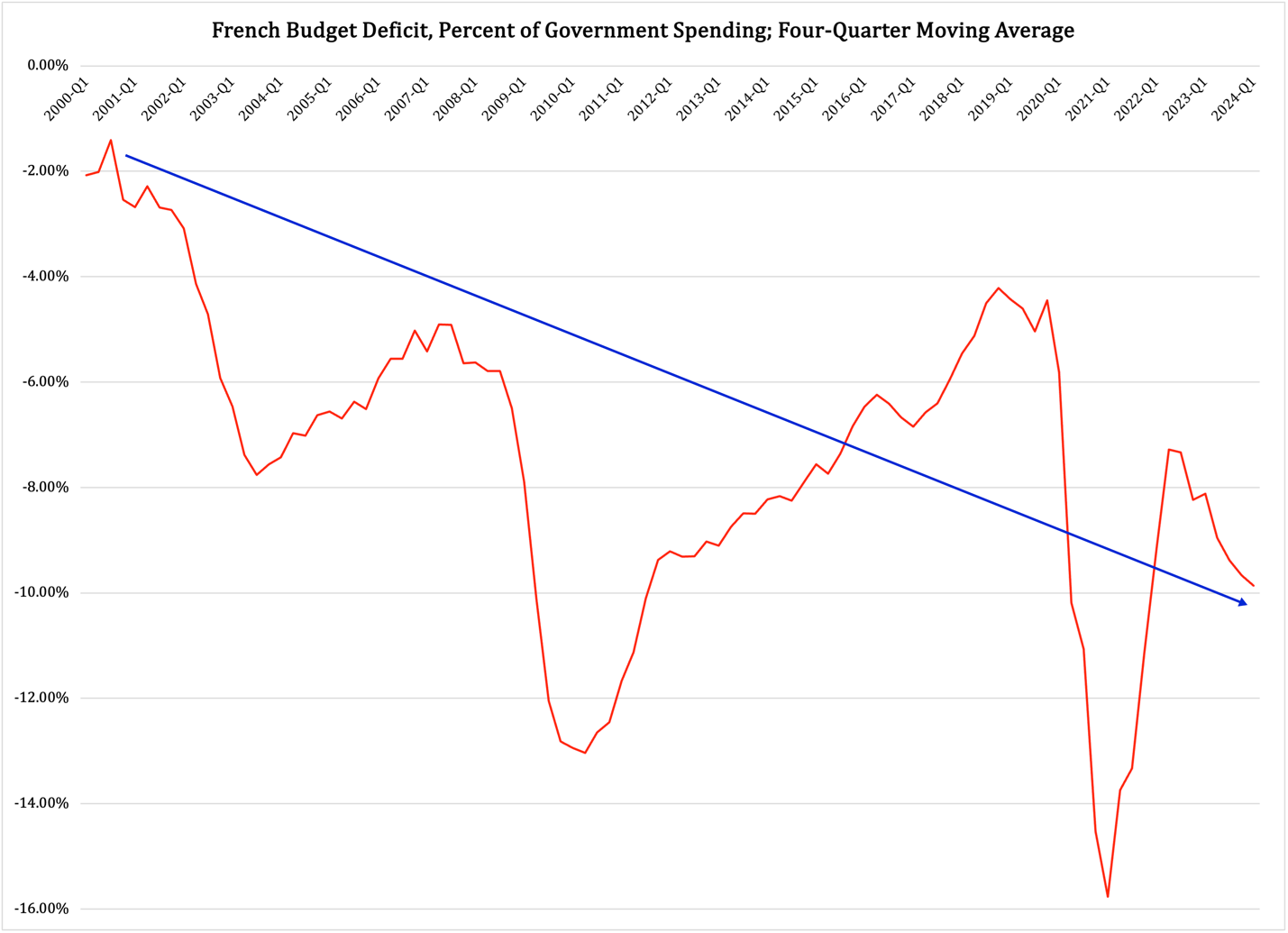

As is visible in Figure 2b, the lack of fiscal fortitude is not new. Here, the blue arrow stretches out from 2001—in the first quarter in which there was almost a budget surplus in the French government finances—all the way to the first quarter of 2024. In other words, despite the volatile nature of the deficit-to-GDP ratio, its long-term trend is one of steadily growing deficits.

Figure 2b

Source of raw data: Eurostat

Source of raw data: Eurostat

Looking at Figures 2a and 2b, one almost gets the impression that French politicians have given up on even trying to balance their government finances. The consequences of this will be dire—and no matter how much the EU would like to ignore it, they are going to have to intervene and enforce their Stability and Growth Pact, SGP, against France.

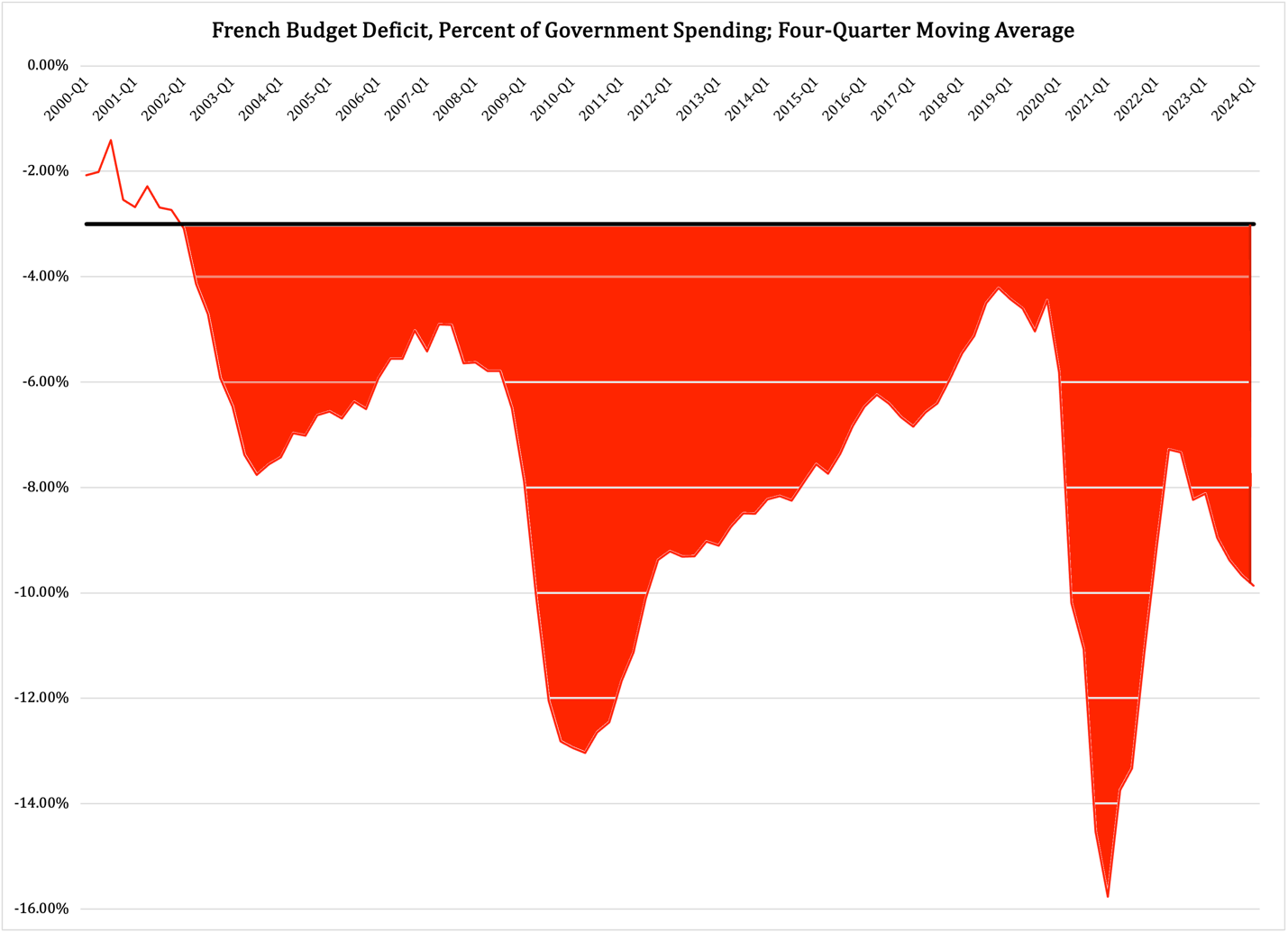

Just to show what an arrogant SGP scofflaw France is, consider the glaring red area in Figure 2c. It marks the budget deficit that exceeds the three-percent-of-GDP limit imposed by the SGP:

Figure 2c

Source of raw data: Eurostat

Source of raw data: Eurostat

Long story short, France has been in breach of the Stability and Growth Pact every year for 22 years. Despite that, the EU has never subjected France to even a remote resemblance of the punitive fiscal measures that they applied against Greece.

This is explainable by the considerable political clout that France has, but from the viewpoint of economic logic, the lack of harsh measures against the French Treasury is glaring. France is the second-largest economy in the euro zone, and its debt—€3.16 trillion—equals 24.4% of the euro zone’s total government debt.

Imagine the speculative contamination that would take place if investors in the euro-denominated sovereign debt market one day decided that France was no longer a credible debtor. If they started selling off even a fraction of their holdings of French government securities, their pessimism would rapidly spread to other, less indebted governments in the EU.

As investors flee the euro zone’s government debt market, they also flee the euro itself. There are people within the currency area who know what this would mean; the fear of an implosion of the euro was a driving reason behind the ECB’s participation in punishing Greece for dragging its fiscal feet in the early months of the 2008-2010 Great Recession.

If a debt crisis hits France, the fallout will be orders of magnitude larger than anything the euro zone risked during the Greek fiscal crisis. And yet, beyond a formal ‘excessive deficit procedure’ letter to the French government, the mighty minds in the EU and the ECB have shown disturbingly weak interest in how notoriously France mishandles its public finances.

Source link : https://europeanconservative.com/articles/analysis/france-europes-next-fiscal-flashpoint/

Author :

Publish date : 2024-10-01 16:04:10

Copyright for syndicated content belongs to the linked Source.