Some content could not load. Check your internet connection or browser settings.

According to the report, “real disposable income [per head] has grown almost twice as much in the US as in the EU since 2000”. A big part of the reason is that the EU has fallen far behind the US (and even China) in the digital revolution. Only four of the world’s top 50 tech companies are European. EU energy prices are relatively high, particularly in comparison with those of the US. EU demographics are also dire. Thus, “[i]f the EU were to maintain its average productivity growth rate since 2015, it would only be enough to keep GDP constant until 2050”. Not least, Europeans are unable to protect themselves, as the war in Ukraine has shown.

The EU cannot change the world. But it can — and should — change itself, to cope with it. What comes out most clearly from this report are the common threads that connect these various ailments. The most important are fragmentation, over-regulation, inappropriate regulation, insufficient spending and undue conservatism. Of these, fragmentation is the most damaging.

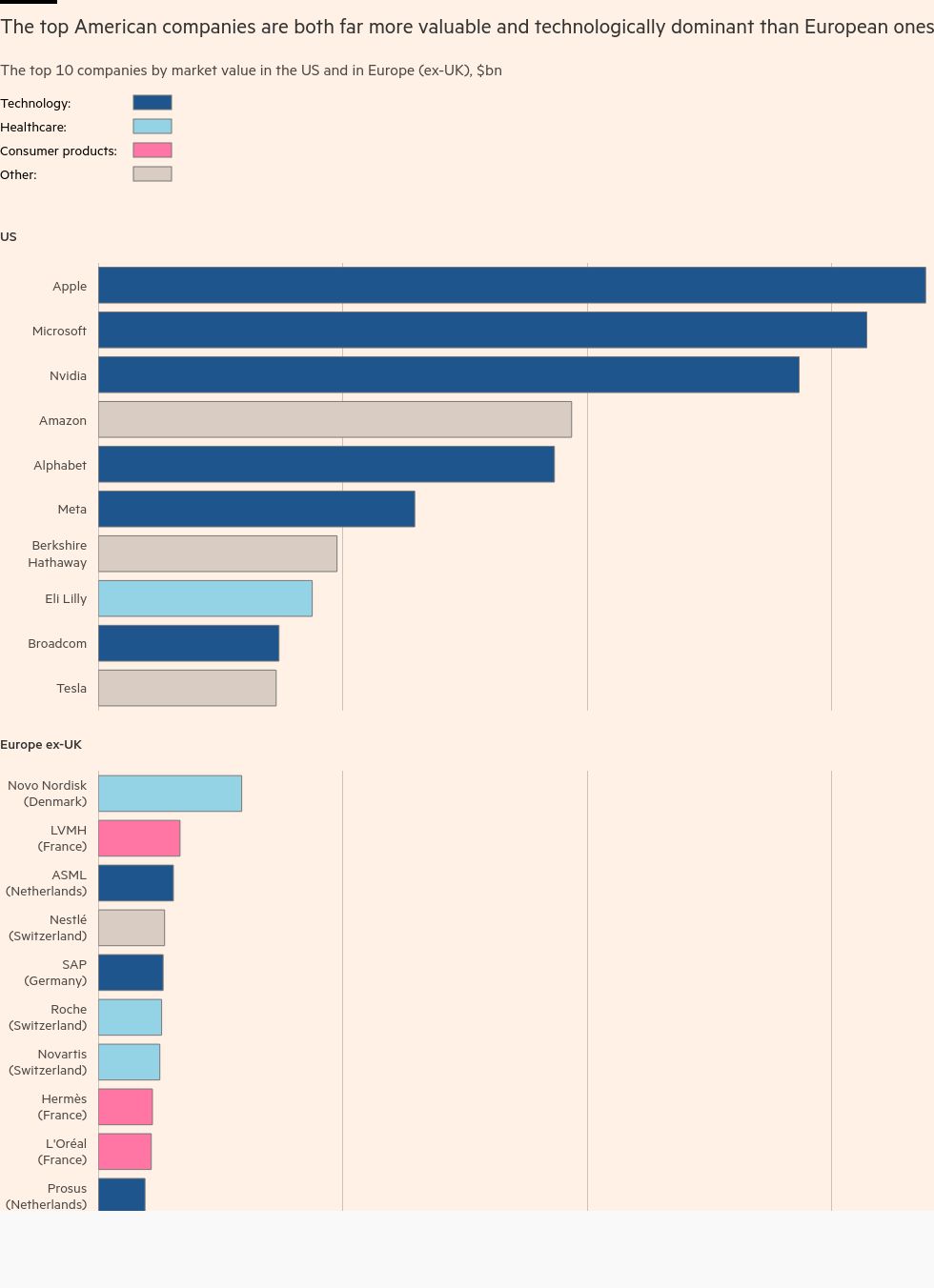

These ills emerge repeatedly in the report. It notes that “Europe is stuck in a static industrial structure with few new companies rising up to disrupt existing industries or develop new growth engines. In fact, there is no EU company with a market capitalisation over €100bn that has been set up from scratch in the last 50 years, while all six US companies with a valuation above €1tn have been created in this period.” Accordingly, the list of the top three investors in research and innovation (R&I) has been dominated by automotive companies for 20 years. Europe risks becoming an industrial museum.

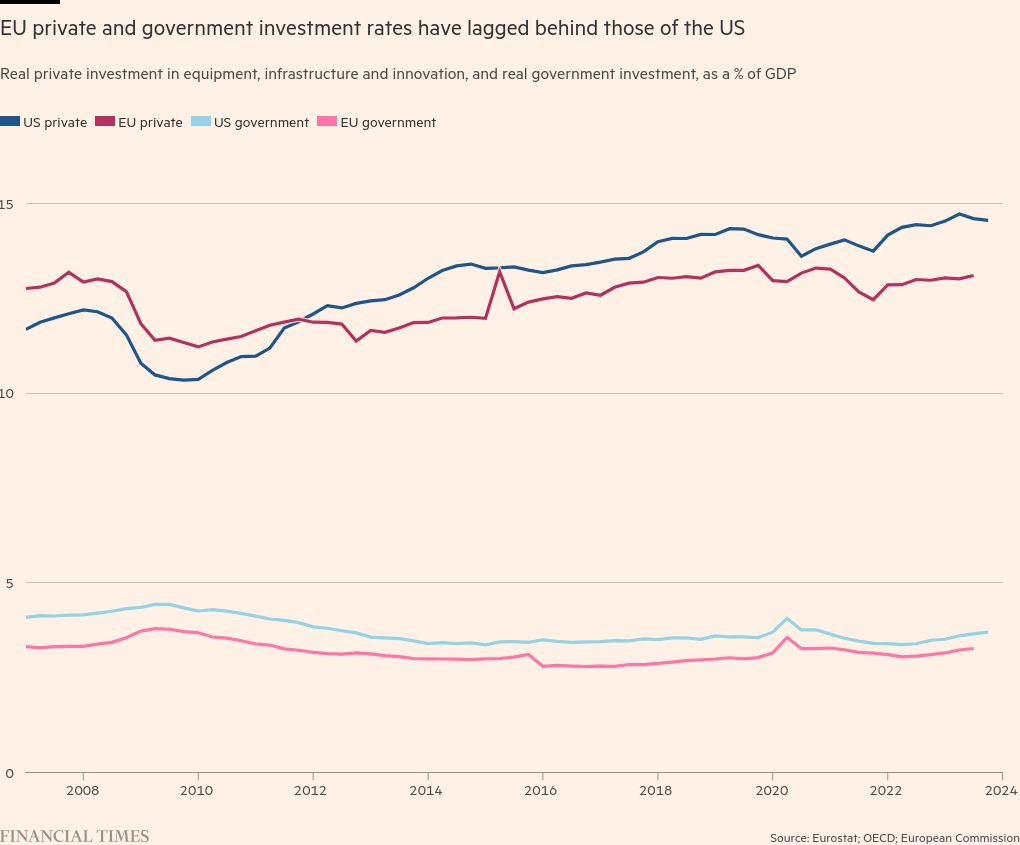

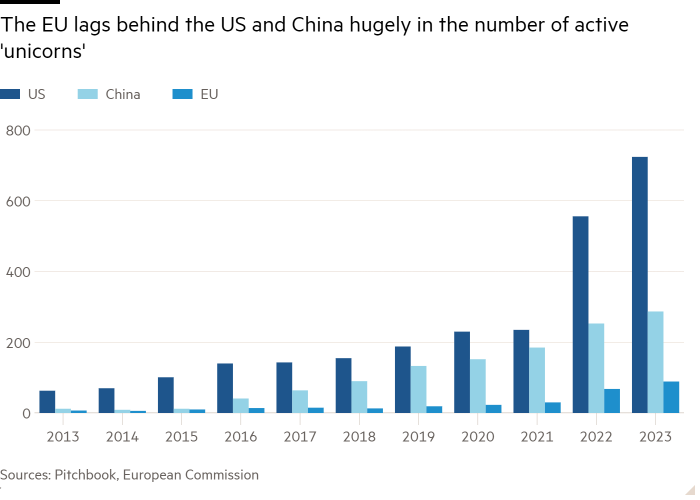

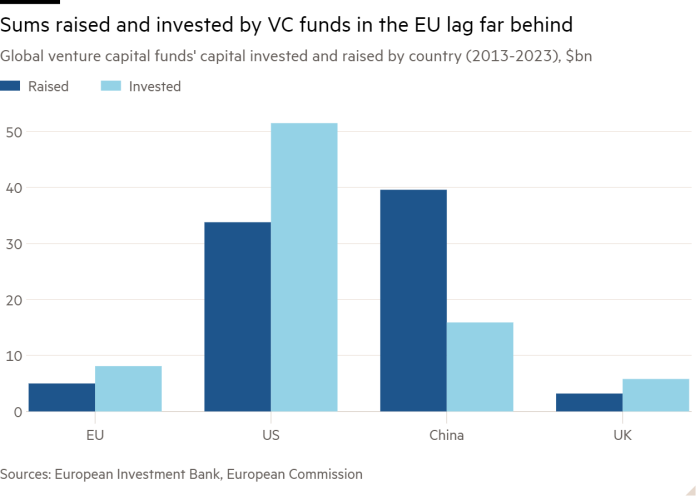

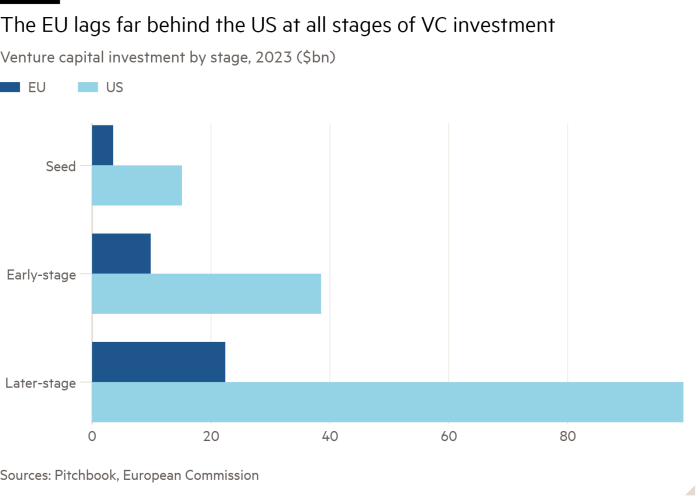

Why? Fragmentation is the main answer. Thus, the single market does not truly exist, in terms of outputs or inputs, especially capital. The university sector is fragmented, too, as is public support for R&I. The lack of scale and risk-taking means that US sources of funds are far greater than those of the EU. As a result, “many European entrepreneurs prefer to seek financing from US venture capitalists and scale up in the US market”.

Over-regulation is also a big problem. This is partly because of excessive conservatism, but also because of the tendency of member states to pile their own regulations on top of the EU’s.

Fragmentation also affects energy and security policy. A fully integrated energy market does not exist, for example. The EU has also failed to integrate either its defence industries or its procurement of military equipment. This raises cost and lowers efficiency. Such fragmentation is unaffordable, especially as the credibility of the US defence commitment comes into question.

Inevitably and rightly, attention is being paid to Draghi’s measured and sophisticated embrace of more interventionist trade and industrial policies. One justification is the concern over security. Another is that the EU is getting an industrial policy anyway, but it is fragmented and spending upon it dominated by the big member countries. The last is that we know that, done properly, industrial policy can improve both competition and global welfare. Who now thinks that creating Airbus was a mistake? It has surely been a triumph. The lesson is that such big interventions should be done together, on a large scale and with clear objectives. Creating a new zero carbon energy system will need all that. So will creation of an effective defence sector.

{kind=link}

Unfortunately, the explanations for many of the problems Draghi describes, notably the fragmentation and conservatism, are also the reasons why his radical solutions are unlikely to be adopted. As he notes, “successful industrial policies today require strategies that span investment, taxation, education, access to finance, regulation, trade and foreign policy, united behind an agreed strategic goal”. For the EU to achieve this will require radical reforms.

Today’s surging nationalism will make implementing such reforms harder still. Europeans are at risk of forgetting the lessons of their past: only if they act together can they hope to shape their future. The British forgot that. Can the others remember — and act?

martin.wolf@ft.com

Follow Martin Wolf with myFT and on Twitter

Letter in response to this comment:

Europe’s capital markets must make it easier to issue equity / From Joseph Harvey, Chief Executive, Cohen & Steers, New York, NY, US

Source link : https://www.ft.com/content/47d28f39-6f9d-4c46-9e36-c45a9f398a62

Author :

Publish date : 2024-09-17 07:00:00

Copyright for syndicated content belongs to the linked Source.